Sidebar

")

Français

Français  Español

Español SINAPS Consult Blog's

Market prospects for fish.

According to 2015 report of OECD/FAO, the year 2014 was characterised by historical peaks in production, trade and fish consumption. Apparent per capita fish consumption is estimated to have reached about 20 kg, with aquaculture overtaking capture fisheries as the main source of fish for human consumption for the first time.

Market situation

The market prospects for fish continue to be positive. The year 2014 was characterised by historical peaks in production, trade and consumption, only slightly affected by events such as the Russian Federation’s import ban and reduced catches in South America.

Apparent per capita fish consumption is estimated to have reached about 20 kg in 2014, with aquaculture overtaking capture fisheries as the main source of fish for human consumption for the first time.

Developing countries, in particular in Asia, will continue to drive major changes and expansion in global fishery production, trade and consumption, being the main producers, exporters and growing consumers. However, in 2014, trade increased faster in developed countries than in developing countries. This is counter to the long-term trend, which has seen developing countries, particularly in South America and South and East Asia, steadily increase their proportion of world trade in fishery products. The major factors behind this reversal were booming growth in the United States market and a record-breaking year for key producer and exporter Norway.

Fish prices grew sharply during the first part of 2014 and weakened during the rest of the year due to softening consumer demand in many European markets and Japan, and improving supply situation of certain fishery species. However, fish prices remained above 2013 levels for most species and products, in particular for farmed species. The FAO Fish Price Index (base 2002-04 = 100) indicates that prices are at record heights reaching a peak in March 2014 (at 164, with aquaculture species at 168).

Projection highlights

The main drivers affecting world fish prices for capture, aquaculture and traded products will be income and population growth, limited increase in capture fisheries production, high meat prices in the short term, and feed prices. All these factors will contribute to high fish prices in the near future followed by a decline in the remaining years of this decade and an increase in the 2020s. In real terms, prices are expected to decline from the record high of 2014. The aquaculture to coarse grains price ratio is expected to be cyclical over 2015-24 and to eventually stabilise slightly lower than the historical average (1990-2014). The price ratio between aquaculture and fishmeal will remain relatively stable. Since the feed demand for fishmeal from aquaculture and livestock sectors is growing faster than supply, an increase in the fishmeal to oilseed meal price ratio is expected. The popularity of the Omega-3 fatty acids in human diets and the growth in aquaculture production have both contributed to a rise in the fish oil to oilseed price ratio since 2012, which is expected to be maintained over the medium term. However, since fish oil and oilseed oil prices are starting from very high levels, a decline is expected in nominal terms for the rest of this decade.

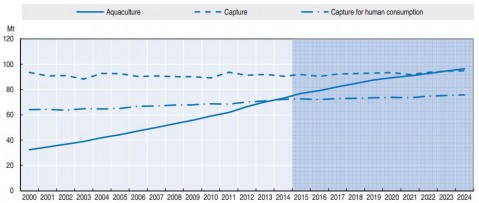

Fisheries production worldwide is projected to expand by 19% between the 2012-14 base period and 2024, to reach 191 Mt. The main driver of this increase will be aquaculture, which is expected to reach 96 Mt by 2024, 38% higher than the base period (average 2012-14) level. Aquaculture will remain one of the fastest growing food sectors, notwithstanding a slowdown of its average annual growth rate going from 5.6% in the previous decade to 2.5% in the projection period. In 2023, aquaculture will surpass total capture fisheries (Figure 1). This development heralds a new era, indicating that aquaculture will increasingly be the main driver of changes in the fisheries and aquaculture sector. Nonetheless, the capture sector will remain dominant for a number of species and vital for domestic and international food security. World production of fishmeal is expected to eventually return to the 5 Mt level by the end of the outlook period and world fish oil production should hover around 1 Mt. In both cases, the share of production of fishmeal and fish oil obtained from whole fish is expected to fall compared to the previous decade.

Figure 1. Aquaculture and capture fisheries

World per capita apparent fish food consumption is projected to reach 21.5 kg in live weight (lw) equivalent in 2024, up from 19.7 kg in the base period. The average annual growth rate will be lower in the second half of the outlook period, due to more competitive meat prices. Per capita fish consumption is expected to increase in all continents, with Asia showing the fastest growth. In contrast with previous Outlook Reports, for the first time, a slight increase is projected for Africa. Lower feed and crude oil prices reduced production and transportation costs enhancing African aquaculture production and imports. Per capita fish consumption will remain higher in more developed economies, even if it is expected to grow more rapidly in developing countries.

Fuelled by sustained demand, innovations and improvements in processing, preservation, packaging, transport and logistics, total fish, and fishery products (fish for human consumption, fishmeal on a lw basis) will continue to be highly traded, representing about 31% of production (36% including intra-EU trade) in 2024. However, global fish trade for human food is projected to grow slower than in the past decade due to increasing domestic consumption by main producers. Developing countries are expected to account for 64% of global fish exports for human consumption by 2024, down from 66% in the base period. Developed regions will continue to remain the main importers.

The key uncertainty for the fish projections remains the productivity gains in aquaculture, which might be affected by several factors, including availability and accessibility to land, water, financial resources, improvement in technology, feeds, etc. In addition, animal disease outbreaks have shown to the potential to affect aquaculture production and subsequently domestic and international markets depending on the size and the species involved. Natural productivity of fish stocks and ecosystem and the occurrence of El Niño are the key uncertainties impacting capture fisheries and also the fishmeal and fish oil outlook. Trade policies, and in particular bilateral trade agreements, remain an important factor influencing the dynamics of the world fish markets.

Extract from:OECD (2015), "Fish", in OECD/FAO, OECD-FAO Agricultural Outlook 2015, OECD Publishing, Paris.

DOI: https://dx.doi.org/10.1787/agr_outlook-2015-12-en

Copyright

© OECD/FAO 2015